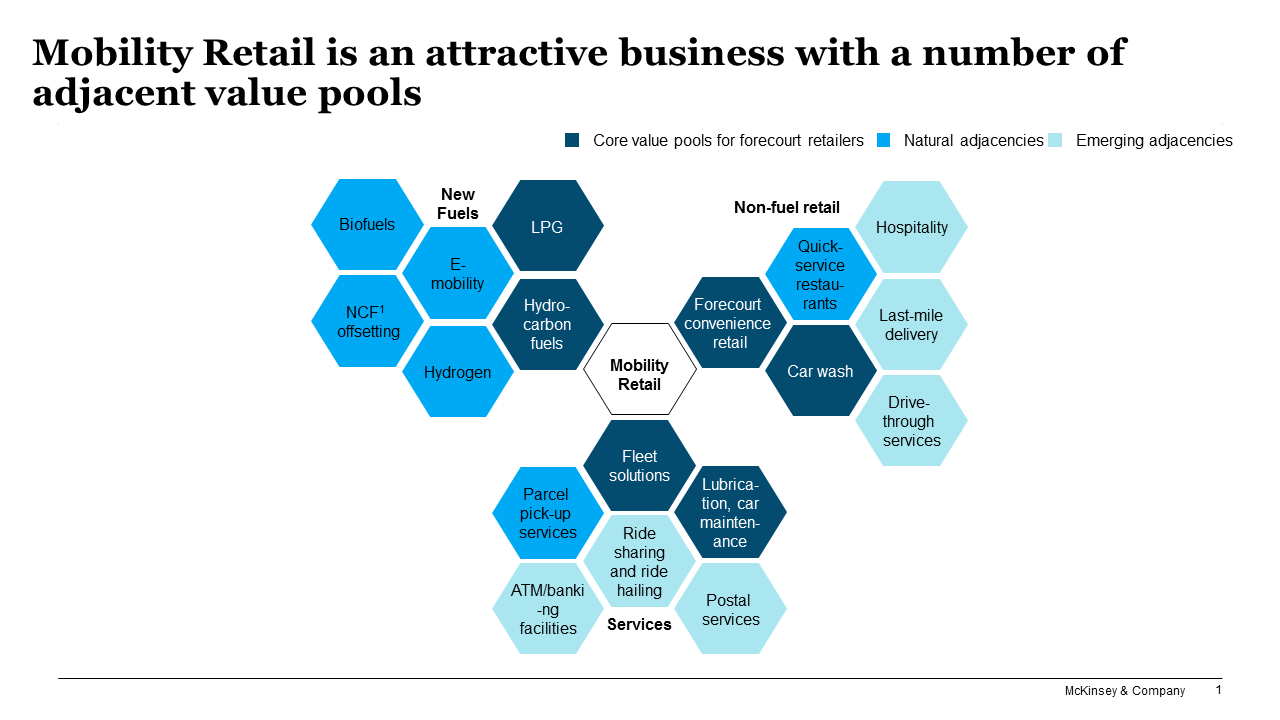

Over the past decade, fuel and convenience retail has been one of the more resilient segments in the oil and gas industry. The growth of both out-of-home consumption and small-format retail has enabled forecourts to capture significant incremental value from convenience retail and other nonfuel retail (NFR) business. As a result, industry asset values have soared. For example, acquisition multiples for US convenience stores have almost doubled—from six to seven times annual EBITDA a decade ago to ten to 12 times today—and now well exceed the multiples of integrated oil and gas companies. Apart from strong profitability, often exceeding 20% ROACE, this is also a result of operators having access to a large number of adjacent value pools allowing them to create multiple customer connections.

Innovative fuel and convenience retailers play across the full space of fuels, convenience and services adjacencies. They cluster their networks according to local customer needs, such as “food to go,” “food for later,” “take a break”, “car care center” or innovative “fleet hubs”. They are also developing new or additional business models; for example, developing forecourts into destinations for food shopping, click and collect, pharmacy and postal services; forming partnerships & alliances to share locations with companies such as McDonald’s and Starbucks; and enabling their customers to interact with them in seamless digital and engaging way.

The industry is offering a lot of exciting developments – in this series of short podcasts we at McKinsey will be bringing insights into industry’s performance as well as ideas for players to get ahead to position themselves for success in this rapidly evolving industry.

Exhibit

Why is the topic of New Mobility retail important now? - McKinsey

Read More

No comments:

Post a Comment